Expanded Home Guarantee Scheme: What Every First Home Buyers Need to Know

- September 12, 2025

- Posted by: admin

- Categories:

For many people living in Sydney, owning a first home has often felt impossible. Every time savings are built up, property prices seem to jump even higher, making the dream of home ownership feel out of reach. On top of the costs, there is stress, uncertainty, and fear that buying a place to call your own will never actually happen. But from 1 October 2025, changes to the Federal Government’s Home Guarantee Scheme mean things could look very different for first home buyers in Sydney.

Understanding the Home Guarantee Scheme

The Home Guarantee Scheme is a government program designed to help first home buyers purchase a property with just a 5% deposit – and avoids the need to pay expensive Lenders Mortgage Insurance (LMI). This means buyers won’t need to spend years saving up a 20% deposit just to get through the door.

What’s Changing from October 2025?

Some of the biggest hurdles first home buyers have faced will be removed thanks to the new rules coming into effect from October 2025. Here’s what’s new:

- No more quotas: Every eligible buyer can access the scheme, not just a limited number of applicants.

- No income caps: High income earners can now qualify.

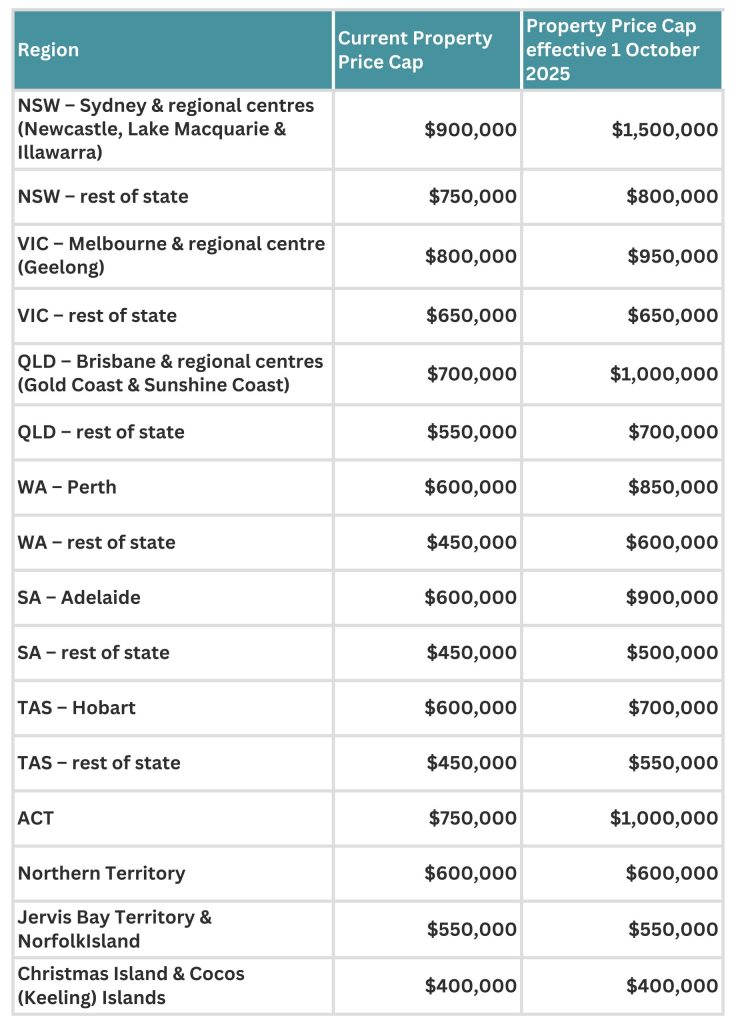

- Increased property price cap: In Sydney, the cap jumps from $900,000 to $1.5 million.

Now, instead of being locked out, many more buyers have a real shot at owning a Sydney home.

Why the $1.5 Million Cap Makes a Big Difference

Sydney’s property prices have always been among Australia’s highest, with the old $900,000 threshold not matching actual market prices. The new $1.5 million limit allows first home buyers to consider a much wider range of properties including townhouses, apartments, and family homes in more sought-after suburbs. Young professionals and families who’ve built decent incomes but haven’t managed large deposits can now look at inner and middle-ring suburbs—places where many people actually want to live.

The Good and the Not-So-Good

Upsides for Sydney First Home Buyers

- Buy Sooner: You won’t need to wait years to save a big deposit.

- Save Money: No LMI could save you tens of thousands of dollars—money that could be used for renovations, emergencies, or investments.

- More Suburbs to Choose From: With a bigger cap, buyers can look at areas that fulfill lifestyle goals—not just the cheapest place they can find.

Important Risks to Consider

- More Buyers, More Competition: By helping more people enter the market, there may be even more competition for homes—and that could push some prices higher.

- Higher Debt, Bigger Commitments: A small deposit means a larger loan and higher monthly repayments, increasing the risk if interest rates rise or your circumstances change.

- Affordability Isn’t Just Borrowing Power: Even if the bank says yes, always double-check that the repayments and lifestyle costs work for you in the long term.

What Should Sydney First Home Buyers Do Next?

- Work Out What’s Affordable: Don’t just chase the maximum loan size. Mortgage repayments should fit within a comfortable budget.

- Think About Lifestyle, Not Just Location: Expanding the property search can help buyers find a balance between a good location and future financial freedom.

- Plan for the Future: Property should be just one part of a bigger financial plan. Make sure it supports your long-term goals, like travel, raising a family, or investing.

How Financial Advice Makes a Difference

A home isn’t just a transaction—it’s a core part of your financial and personal life. A professional adviser can help buyers:

- Ensure repayments are affordable, so there’s still room to enjoy life.

- Weigh up choices like starting a family or prioritising investments.

- Decide if it’s better to buy now, wait, or try a different strategy.

What are the Property Price Caps?

Frequently Asked Questions

What is the Home Guarantee Scheme?

It is a Federal Government initiative to help first home buyers get into the property market with a minimum 5% deposit and no LMI payments. From October 2025, the rules are even more open with no quotas, no income caps, and a higher price limit.

How much can someone borrow under the new scheme?

Buyers in Sydney can purchase properties up to $1.5 million, though responsibility is needed since a bigger loan means higher repayments and risk.

How much money can be saved by avoiding LMI?

LMI can cost from $20,000 to $60,000 or more in Sydney, so going without it is a major saving that could be used to improve or protect your new home.

Will the scheme push house prices even higher?

There’s a chance. With more buyers able to compete for property, some suburbs could see more price growth—but that doesn’t change the need for smart, considered buying decisions.

Final Thoughts

The expanded Home Guarantee Scheme for Sydney first home buyers is a fresh opportunity—and a reason for optimism for those who’ve struggled to break into the market. It offers an easier way in, but doesn’t remove all the risks. By combining the scheme’s benefits with good financial advice and realistic planning, first home buyers in Sydney can step into home ownership with clarity, confidence, and a strong financial future. For more details call us on 0403 803 470.